Fitch Ratings: Fitch Ratings believes a sustained period of US dollar (USD) strength against emerging market (EM) currencies could weigh on some EM sovereign credit profiles, potentially softening the current positive ratings momentum for EMs. Most at risk in such a scenario – which does not form part of our base case for 2024-2025 – would be sovereigns that experience large and durable depreciation against the dollar or large declines in official foreign reserve buffers, and that have a large share of their debt denominated in foreign currencies.

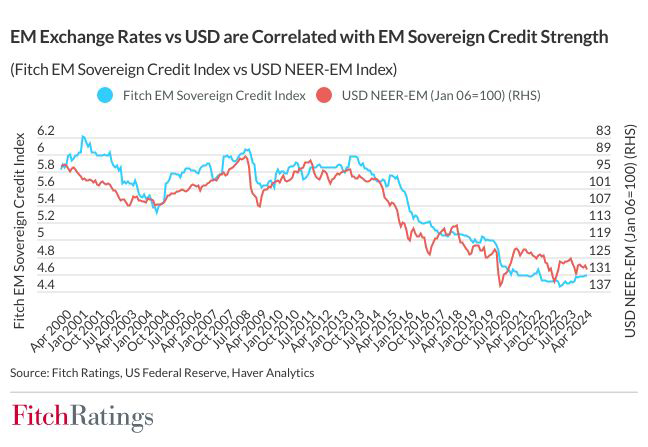

The nominal effective exchange rate of EM currencies against the USD has historically been strongly correlated to EM sovereign ratings, with a stronger USD being associated with weaker EM credit profiles. We believe this relationship is likely to remain robust in 2024-2025 if the USD experiences a period of sustained strength.

Nonetheless, the net balance of rating Outlooks for Fitch’s EM sovereign portfolio as a whole is currently Positive, reflecting prospects for improvement in many of the credit profiles. The picture varies regionally, with Emerging Europe and Latin America both having a relatively large number of EM sovereigns on Positive Outlook, and Asia having more sovereigns on Negative Outlook than Positive.

Ratings of EM commodity importers and smaller and frontier EMs remain significantly weaker than before the Covid-19 pandemic, so some credit profiles may have room to improve as pandemic-related economic and fiscal scarring fades and global activity normalises. EM exchange rates, in aggregate, were also relatively stable against the USD over 4M24, compared with the USD’s stronger appreciation against some developed market currencies, including the yen and Swiss franc. We believe this contributed to the overall strength of EM prospects. Still, a number of EM currencies did weaken somewhat over 4M24, including Brazil’s real and some Asian currencies.

Fitch’s baseline assumption remains that US Treasury yields will fall over 2024-2025 as the Federal Reserve begins to cut rates. This should allow more EM currencies to appreciate against the USD. Nonetheless, the resilience of the US economy and, in turn, the persistent inflationary pressure there have highlighted risks to this outlook. If US rates remain at a high plateau – or rise even further – this could result in sustained USD strength, with potential adverse consequences for some EM credit profiles.

We view EM sovereigns with larger shares of USD-denominated debt as being more exposed to exchange rate risks, as depreciation against the dollar increases the burden of debt repayment in local-currency terms. External government debt exceeded 50% of GDP in 2023 for nine Fitch-rated EM sovereigns – all in the speculative ‘B’ rating category or lower – and was over 30% for a further 27.

We view EM sovereigns with larger shares of USD-denominated debt as being more exposed to exchange rate risks, as depreciation against the dollar increases the burden of debt repayment in local-currency terms. External government debt exceeded 50% of GDP in 2023 for nine Fitch-rated EM sovereigns – all in the speculative ‘B’ rating category or lower – and was over 30% for a further 27.

Generally, we believe larger, sustained devaluations are accompanied by a higher danger of social and economic instability, particularly linked to accompanying inflationary effects. Consequently, risks to sovereign credit profiles can be greater, with large-scale bouts of depreciation that last for a year or more.

As of 1 May, several Fitch-rated EMs had seen yoy deprecation against the USD of over 30%, including Angola (B-/Stable), Argentina (CC), Egypt (B-/Positive), Nigeria (B-/Positive), Turkiye (B+/Positive) and Zambia (Restricted Default). However, there may also be considerations that mitigate the impact, for example, where depreciation is a result of broader economic adjustments that improve long-term economic prospects, or is a condition of financial support from the IMF or other lenders. Such considerations contribute to the Positive Outlooks on the ratings of Turkiye, Egypt and Nigeria.

The post Risk of Stronger US Dollar Could Affect Emerging Market Credit Momentum appeared first on Adaderana Biz English | Sri Lanka Business News.